Krisanapong Detraphiphat/Getty

- An APR is the cost of borrowing money, stated as a yearly rate.

- You can use APR to compare loan offers because it shows what you'll repay in interest, plus fees.

- APRs can be fixed or variable, and calculated as simple or compound interest.

- Visit Insider's Investing Reference library for more stories.

When you use a credit card or take out a loan, your lender will charge you interest for the privilege of borrowing the money. They'll typically present this cost as an annual percentage rate, or APR, which shows your total cost of borrowing – plus fees. Because they help you compare offers and find the best deal, it's important to know how they work.

What is APR?

An APR is the cost of borrowing money expressed as a yearly rate. While the APR is usually applied to consumer debt, like credit cards and loans, it can also represent the return on an investment you make.

"In most cases, [it's] the single most important factor to understand when both borrowing or saving money," says Brian Stivers, an investment adviser and founder of Stivers Financial Services in Knoxville, Tennessee. That's because it helps you "understand the true cost of borrowing money and not just the monthly payment."

For instance, you can use APRs to compare the borrowing costs on a mortgage. Let's say Lender A and Lender B both offer an interest rate of 2.75% and quote you a list of fees you'll pay on the loan.

It can be tough to compare those fees because they may go by different names – plus, you'll have to crunch the numbers. But the APR takes those fees, along with the interest rate, and translates the information into a unit you can quickly measure. In this example, let's say Lender A charges an APR of 2.90%, while Lender B quotes an APR of 3.50%. At a quick glance, you can tell Lender B's loan includes more costs outside of what you're borrowing.

| Lender A | Lender B | |

| Interest rate | 2.75% | 2.75% |

| APR | 2.90% | 3.50% |

While the 0.60% difference may seem insignificant in this example, it can really add up if you're borrowing a large sum of money - like a mortgage, for example.

| APR | 30-yr mortgage | Monthly payment | Total mortgage | |

| Lender A | 2.90% | $300,000 | $1,249 | $449,528 |

| Lender B | 3.50% | $300,000 | $1,347 | $484,968 |

In the example above, that 0.60% difference means you'd pay $35,440 more if you'd went with Lender B. This is the power of APR.

That being said, it's always a good idea to calculate the interest you'll pay over the life of a loan when the interest rates are different. You might end up paying less interest on a loan that has a higher APR, and you'll have to figure out if the higher fees are worth it.

How does APR work?

On a loan, APR includes the interest rate plus any fees the lender charges, such as origination, legal, or underwriting fees. APR isn't so complicated on a credit card - it's just the interest rate stated as a yearly rate.

The APR was designed to give borrowers more information about what they're really paying to borrow money. Thanks to the federal Truth in Lending Act (TILA), lenders are required to disclose the APR on every consumer loan agreement before the borrower signs the contract. The TILA disclosure also includes other important terms, including:

- Finance charge, or the cost of credit expressed as a dollar amount.

- Amount financed, which is typically the dollar amount you're borrowing.

- Payment information, such as the monthly payment, the total number of payments you'll make, and the sum of all your payments combined (which includes principal plus financing costs).

- Other information, such as late fees and prepayment penalties.

When you apply for the loan and receive the TILA disclosure, it might be written into the loan contract. It's a good idea to review the whole contract and make sure you understand the terms before signing on the dotted line.

How is APR calculated?

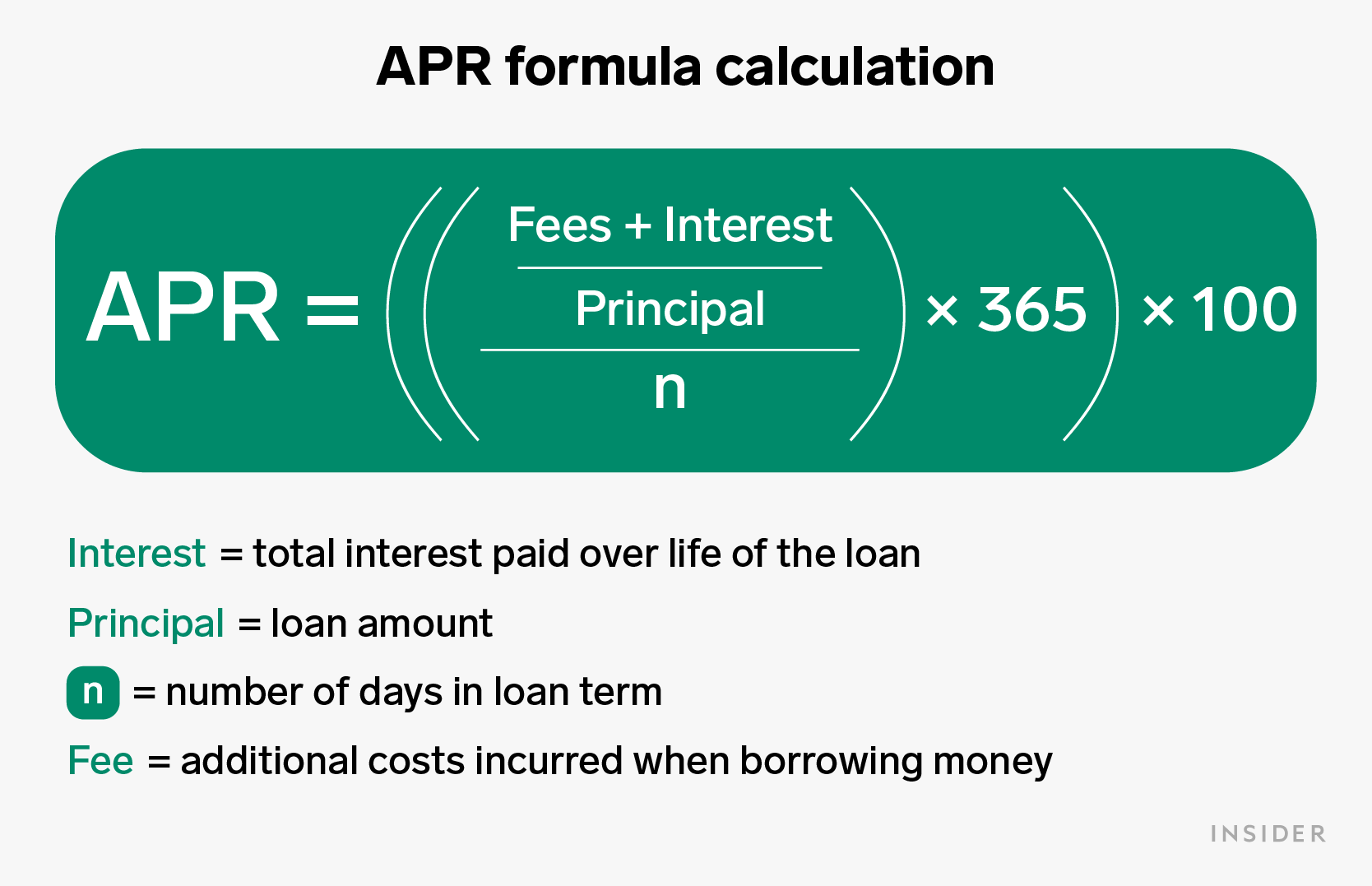

The formula for calculating APR is as follows:

Where n = number of days in the loan term.

Check out one example to see how it works. Let's say you take out a $5,000 personal loan with a two-year loan term and a $400 origination fee. The total interest you pay over the life of the loan equals $980. Follow these steps to calculate the APR:

- Add up the fees and interest: $400 + $980 = $1,380

- Divide that number by the principal, or the amount you're borrowing: $1,380/$5,000 = 0.276

- Divide by the number of days in the loan term: 0.276/730 = 0.00037808219

- Multiply what you've got by 365: 0.00037808219 x 365 = 0.138

- Now multiply by 100 to find the APR: 0.138 x 100 = 13.8%

What is a good APR?

A good APR is simply one that's affordable to you, but there are some general rules you can follow when shopping around. For instance, the National Consumer Law Center says APRs over 36% are unaffordable.

But it also depends on the type of financial product and loan term. The APR on an auto loan might be higher than one on a mortgage, but the longer term on a mortgage means you'll likely pay more interest over time.

APR varies with the type of financial product you're taking out, but it also depends on the lender's overhead costs. For example, an online lender often has lower expenses than a large bank with brick-and-mortar locations. "With lower expenses, they can generally charge less APR to achieve their profit margin," Stivers says, "than a larger lending institution with many locations and more employees."

APR vs. APY

Here's what to know when comparing APR with APY:

| APR | APY |

|

|

APR vs. interest rate

Some people think the APR and the interest are one and the same, but they have different meanings when it comes to loans. "Interest rates only reflect the percentage of interest charged on the loan," Stivers says. "The APR includes additional costs associated with the loan."

Some of these additional costs include discount points, loan origination fees, and other underwriting fees.

Here's a good way to think about it: You'll use the interest rate to calculate your monthly payment, and use the APR to help gauge the entire cost of the loan and compare offers.

Types of APR

Several credit products, like mortgages and auto loans, only come with one APR. The APR may be fixed, which means it never changes, or variable, in which it may go up or down over time.

Other types of debt, like credit cards, may charge several APRs. That's because "lenders, in general, have different APRs for different risk," Stivers says. "For example, a balance transfer from one credit card to another generally has lower risk since there is a history of the consumer paying the payment to the original credit card company. So, the new credit card may discount their APR due to the perceived less risk than a brand-new purchase with no payment history."

A credit card may charge a different APR based on the type of transaction you're doing:

- Purchase APR: applies to the purchases you make with the credit card. "Credit card companies will often use a lower APR, sometimes 0%, for a short period of time - six months to one year - to entice a consumer to use their credit," Stivers says.

- Balance transfer APR: applies to debts you transfer to your credit card. Some credit cards offer a low promotional APR on balance transfers.

- Cash advance APR: applies when you borrow cash against the credit line. This APR is usually higher than the purchase APR.

- Penalty APR: applies when you make a late payment or miss one entirely. The credit card issuer has to follow certain rules before applying a penalty APR to your account.

- Introductory/promotional APR: a low APR that applies to certain transactions - like purchases or balance transfers - for a limited amount of time. The time frame varies with each card but is usually anywhere from 12 to 18 months.

Keep an eye on your credit card balance when it comes with a promotional APR, though. "The credit card companies realize few consumers will pay off the debt in the allotted time," Stivers says, "and will then raise the APR to much higher rates at the end of the promotional period of time."

The financial takeaway

Annual percentage rate is a helpful way to measure the total cost of borrowing. On a loan, it's based on the lender's interest rate plus fees they charge, while on a credit card it's simply the rate expressed as a yearly rate. It's important to know the APR before taking out a credit card or loan because you can use this number to compare offers - and finding the best deal can help you save money.