With almost a month gone since it began life as a public company, analysts are warming to Snapchat’s parent company, Snap Inc.

A number of investment banks recommended buying the stock at the start of this week, with price targets in the high-$20 range.

UBS analysts Eric Sheridan, Alexandra Kasper and Bridget Han took a more measured approach, applying a forward-looking neutral rating.

In a research note titled “Are Ghosts Real?”, the analysts outlined set out three key questions that will be crucial for Snap’s prospects over the next 12 months.

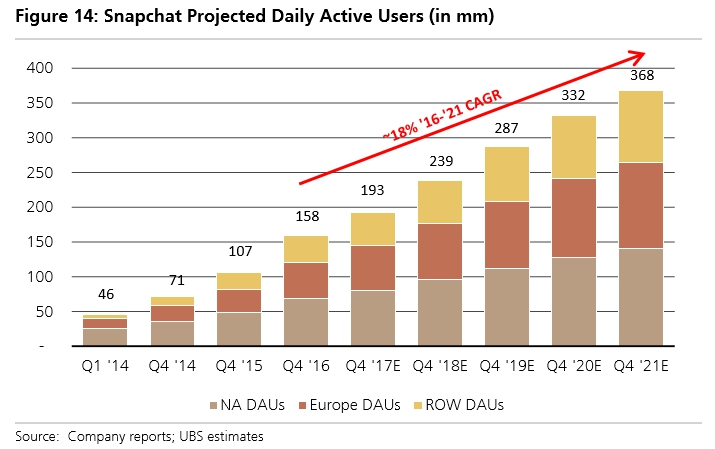

1. Can Snap scale up to 250 million daily active users (DAUs) over the next 3 plus years?

The UBS analysts say this is likely, as the company has demonstrated a focus on gaining users in developed markets with mature advertising sectors.

In addition, they note time spent on mobiles is on the rise and data costs are falling. Snapchat's origination as a "mobile first platform" means it has a strategic advantage in the overall shift towards mobile contact.

This chart shows past user numbers and the UBS analyst's predictions for Snapchat growth between North America, Europe and the rest of the world:

In order to meet future growth targets, UBS has outlined growth in the 35+ age demographic as a key focus area.

While Snap gains advertising benefits from its young user base (such as the ability to spend more time on the app, and quick adoption of digital content), the purchasing power of older demographics is also of key interest to advertisers. This chart shows the current breakdown of Snap's users:

The analysts cite heightened competition as a risk to Snap's future growth targets, with the advent this week of Facebook's Stories feature as a direct competitor.

Snap is strategically focused on measured growth in its user base while placing a premium on the user experience. UBS highlighted comments from company founder Evan Spiegel at the Snap IPO presentation, who said that "bigger isn't always better". DAUs currently spend about 25-30 minutes a day on the app.

2. Can Snap achieve ad monetisation of $US5-10 billion of revenues over the next 3-5 years?

UBS thinks it can. The analysts view Snap as an under-monetised platform which provides compelling content for advertisers and the ability to further innovate in the advertising space.

Snap stands to benefit from the continued shift in advertising, away from the traditional TV medium to digital video content.

"Specifically, based on SMI US agency billings data, ad spending for digital video has continued to grow mid-to-high double digits over the last few quarters while TV ad spending was down to up low single digits over the same period".

The chart below shows just how significantly UBS expects Snap's advertising revenue to grow over the next five years:

With 96% of its revenue obtained from advertising, the analysts say Snap's revenue is driven by two key areas - "1) Sponsored Creative Tools, including Sponsored Geofilters and Sponsored Lenses and 2) Snap Ads".

Sponsored Creative Tools allow advertisers to directly engage with user content, either by customised photo filters (Geofilters) or "interactive lenses that can be overlaid on a person's face or their surroundings" (Lenses). Snap Ads provides the opportunity to strategically place advertising within a user's Snap story.

A unique feature of Snap Ads is that they are watched with the sound on 60% of the time, which creates extra value for advertisers. The UBS analysts expect Snap Ads to become a more significant driver of advertising revenue than Sponsored Creative Tools.

3. When will Snap's operating leverage allow the company to become profitable?

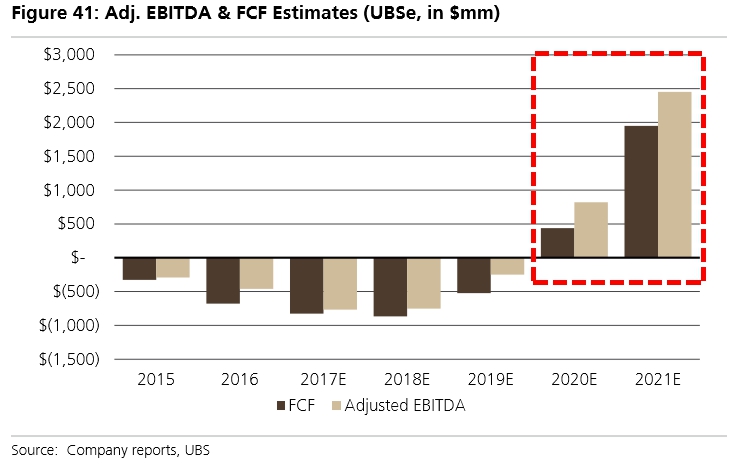

UBS expects Snap to become free cash-flow (FCF) positive by 2020.

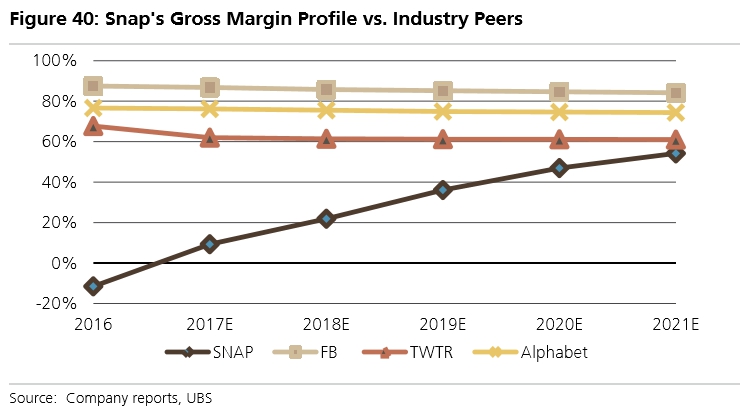

They note that Snap's current gross profit margins are pressured because instead of building its own infrastructure investments for cloud storage and computing costs (like competitors such as Facebook), Snap has outsourced this capacity to external servers.

"Specifically, Snap has committed to spend ~$2bn with Google Cloud over the next five years and ~$1bn with Amazon Web Services (AWS) over the same timeframe."

The unique structure "should allow for a more fixed cost curve in outer years". See here:

As Snap continues to grow its base and extend user engagement, the UBS analysts "expect to see significant leverage in the out years from incremental revenue growth (per DAU) against a flattening COGS per user curve."

In other words, Snap will start making money in 2020. See below for the five-year projections for FCF and adjusted earnings before interest, tax, depreciation and amortisation (EBITDA).

Factoring in the 3 key areas above, the analysts' model calculates a 12 month price target for Snap of $US24 with a neutral rating.

Snap shares closed down 6.8% in US trade overnight at $US22.21.