Happy election day eve. I’m Megan, the healthcare team’s startups and venture capital reporter. I’m filling in for Lydia, who’s still on her cross-country move to Colorado. I’m covering a lot these days, but I’m been particularly interested in digital health startups that employ gig workers.

Analysts from Rock Health, a healthcare venture and advisory firm, told Blake Dodge that the flurry of digital health initial public offerings in 2019 and 2020 was no fluke, according to a July report.

At least nine such companies have gone public in the last 17 months, including Livongo, Health Catalyst, Change Healthcare, Peloton, and Hims.

The firm is keeping a running list of companies that are ripe for an IPO, given their funds compared to the average amount for a digital health startup pre-IPO, which is $187 million.

Curve, a remote monitoring and emergency care startup that works with patients in nursing homes and assisted living facilities, raised $6 million in seed funding on Thursday.

Curve founder Dr. Timothy Peck also founded Call9, a similar senior care startup that shut down in 2019 after being unable to secure payment from patients with Medicare.

This time around, Peck said he recognized that he needed a senior leadership team around him to lead Curve as demand for remote patient monitoring for at-risk populations rose with the pandemic.

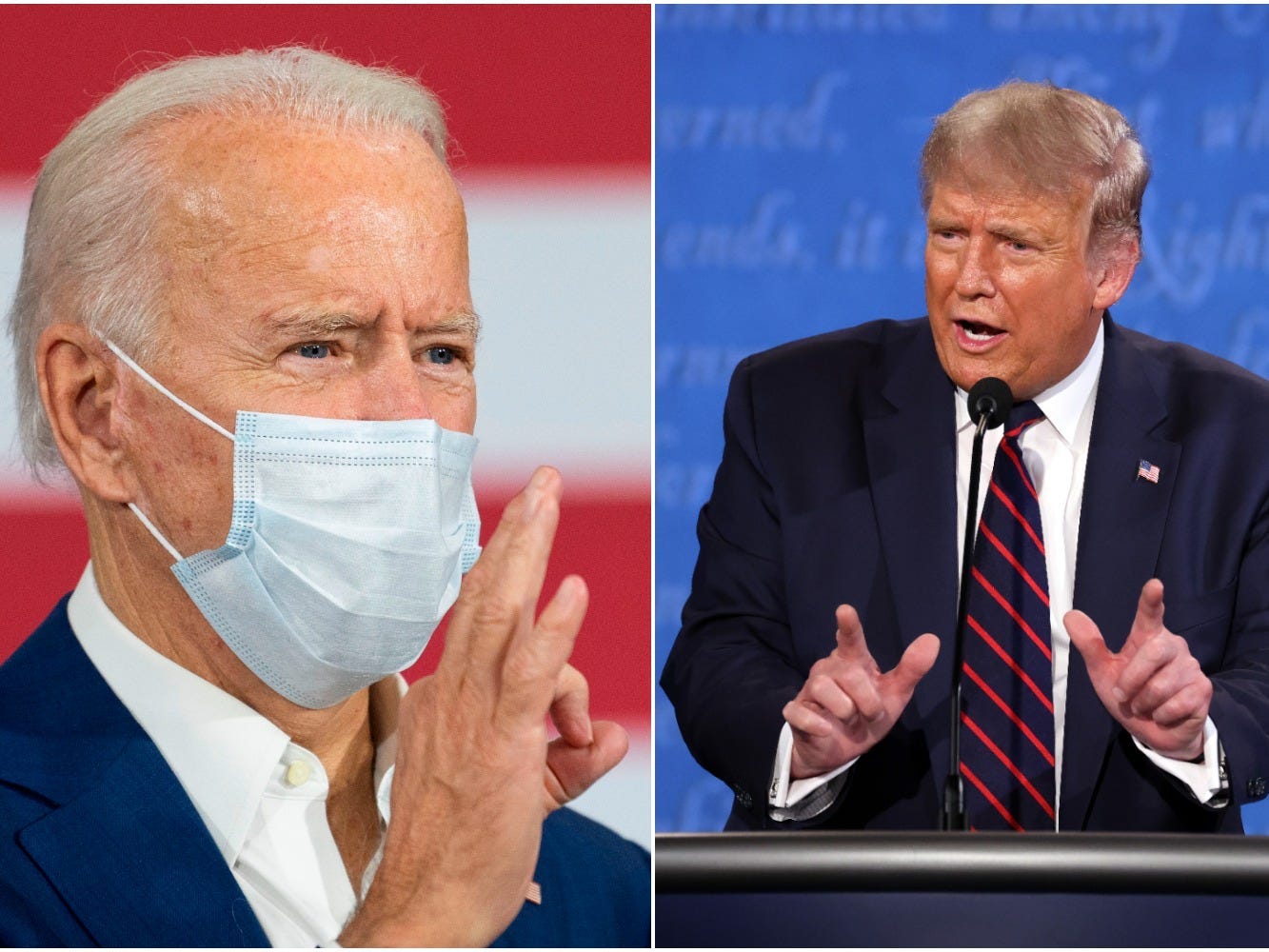

Healthcare executives are favoring Democratic presidential candidate Joe Biden when it comes to their personal campaign donations, an Insider analysis has found.

Insider reviewed campaign-donation disclosures linked to 100 major healthcare companies this election cycle and found that CEOs from Merck, Independence Blue Cross, and Kaiser Permanente were among the largest contributors to Biden.

Biden has promised to raise taxes and overhaul the healthcare system partly by controlling prescription-drug prices and health-insurance costs. But that hasn't stopped healthcare bosses from choosing him over President Donald Trump.