Saudi Arabia’s national debt ballooned during the two years of lower oil prices.

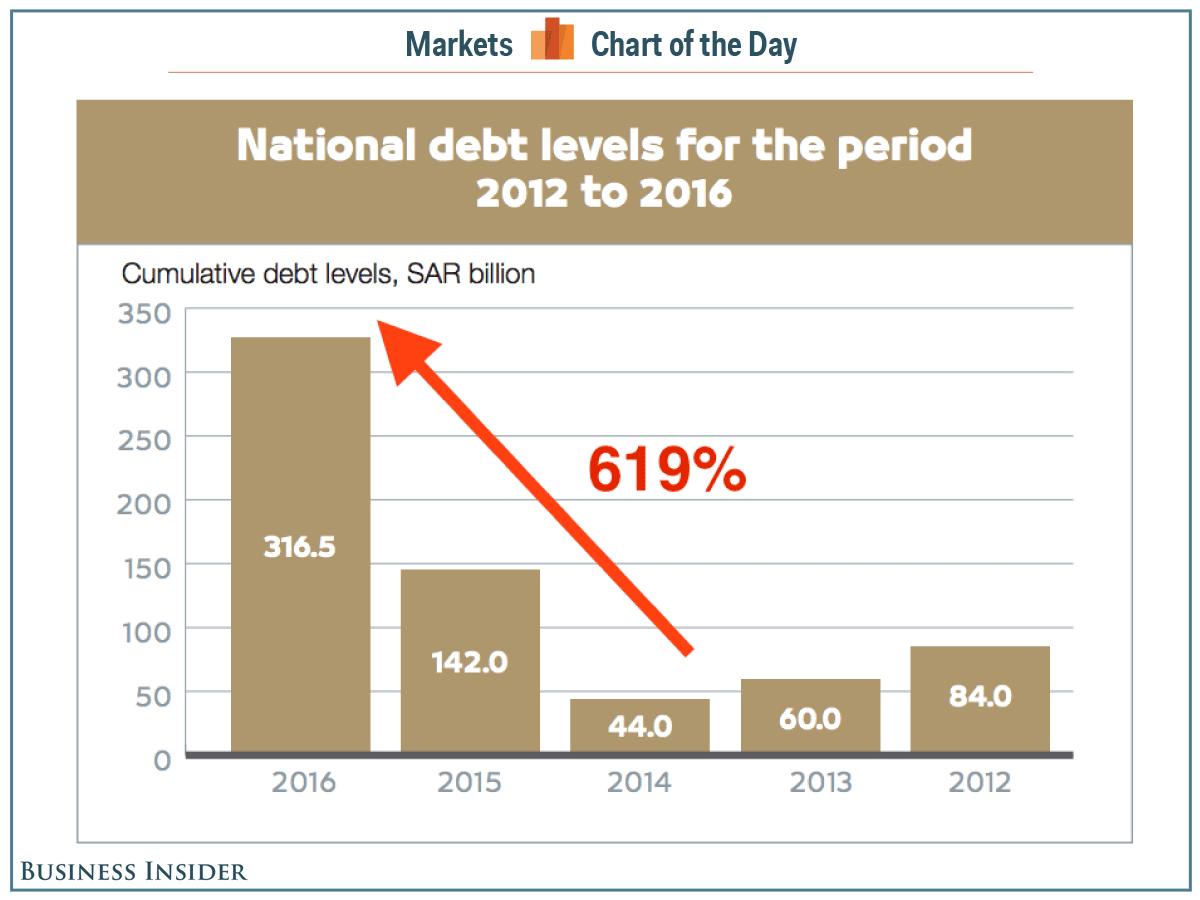

The kingdom’s national debt rose to 316.5 billion riyals in 2016 (about 12.3% of the projected GDP in fixed prices for 2016), up from 142.0 billion in 2015, according the Ministry of Finance’s 2017 budget report.

Moreover, the national debt has increased by about 619% from 2014 – the year OPEC decided not to cut production, after which oil prices plummeted – to 2016.

You can see the rise in debt in the chart shared by the Saudi Ministry of Finance in their report. Note that the x-axis goes from right to left.

Saudi Arabia, one of the world's big oil players, has been feeling the burn of lower oil prices over the past two years.

But in 2016, the kingdom has started pushing forward with spending cuts and reforms and has been working on curtailing its "addiction" to oil via the Vision 2030 plan.

In fact, back in September, the Saudis announced several fiscal-consolidation measures, including cutting ministers' salaries by 20% and canceling bonus payments for state employees, in an effort to reduce its record budget deficit.