- Recent filings from a lawsuit against Elon Musk suggest that he testified that he is “financially illiquid,” despite an estimated $23.7 billion net worth.

- Top corporate executives like Musk often receive most or even all of their compensation in the form of potentially illiquid stock or options in the companies they lead, rather than in cash.

- A May report from The New York Times indicated that the Tesla CEO received stock options worth nearly $2.3 billion in 2018 – but the electric-car maker disputed that claim, saying Musk “actually earned $0 in total compensation from Tesla in 2018.”

- The discrepancy comes from the pay being calculated in accordance with Securities and Exchange Commission rules on CEO-compensation reporting, as opposed to the actual value realized by executives in any given year.

- The structure of Musk’s compensation plan is also a factor, and the Tesla CEO won’t personally realize any value until the company hits some extremely ambitious performance goals, including revenue and profitability targets that could be updated after next Wednesday’s earnings filing.

- Visit Business Insider’s homepage for more stories.

Elon Musk is reportedly low on cash, despite his multibillionaire status. And one reason for that dichotomy is the way top executives often get paid.

Musk is facing a defamation lawsuit from a British diver whom he referred to as a “pedo guy” on Twitter last year. A Bloomberg report on Wednesday said that filings in the suit indicate that Musk told the diver’s lawyers he was “financially illiquid,” or short on cash or easily sold assets.

Even though Musk has a net worth of about $23.7 billion, according to Bloomberg, most of that wealth is tied up in Musk’s massive holdings in Tesla and SpaceX stock. Those holdings may be difficult or even impossible for Musk to quickly sell for cash, meaning it’s quite possible that he could face a liquidity crunch.

It’s not uncommon for top executives like Musk to be paid largely in potentially illiquid stock or options in the companies they lead. Indeed, Musk has refused his cash salaries from Tesla and received nearly all his compensation from that company in the form of stock.

Musk's situation is even more complicated than a typical CEO's. A May report in The New York Times indicated that Musk made $2.3 billion in 2018 as the CEO of Tesla - but according to the company, he actually earned $0 that year.

Under the terms of Musk's compensation agreement with the electric-car maker, the CEO will earn a massive payday once the company achieves some stunning stock-price and financial goals. Some of those financial milestones have been achieved, but the stock-price objectives remain miles away.

Next Wednesday's earnings results will provide an update on how far Tesla needs to go to hit the next set of revenue and earnings milestones Musk needs to achieve before benefiting from the compensation package.

Confused yet? The intricacies of Musk's compensation package with Tesla is an illustration of the surprisingly difficult task of figuring out how much CEOs get paid.

The key to the discrepancy between the 2018 compensation figure and Musk's actual earnings of $0 is in how pay is calculated according to the Securities and Exchange Commission's rules for reporting CEO compensation, as opposed to what top executives actually gain in a particular year.

Many CEOs receive most of their compensation in the form of shares or stock options to buy shares at a given price and time. Often, those stock or option grants don't vest or become available to the CEO until some amount of time has passed - or, as in Tesla's case, some set of performance goals are met.

That makes measuring exactly how much a CEO makes in a given year surprisingly hard to quantify.

Getting technical about executive compensation

The Times published a ranking of the compensation of 200 CEOs of major companies in 2018 based on an analysis by the executive-compensation consulting firm Equilar.

One of the most stunning results was the reported compensation for Musk. According to The Times and Equilar, the Tesla CEO received stock options estimated to be worth nearly $2.3 billion in 2018. Musk's reported compensation was more than 17 times that of the next-highest executive on the list, Discovery Communications CEO David Zaslav.

However, after Business Insider highlighted Musk's eye-popping compensation, Tesla reached out to us through a representative and disputed this characterization.

Here's Tesla's statement:

"Elon actually earned $0 in total compensation from Tesla in 2018, and any reporting otherwise is incorrect and misleading. Unlike other CEOs, Elon receives no salary, no cash bonuses, and no equity that simply vests by the passage of time. His only compensation is a completely at-risk performance award that was specifically designed with ambitious milestones, such as doubling Tesla's current market capitalization from approximately $40 billion to $100 billion. As a result, Elon's entire compensation is directly tied to the long-term success of Tesla and its shareholders, and none of the equity from his 2018 performance package has vested."

According to the proxy statement, under the terms of the company's 2018 compensation plan for Musk, the CEO would receive a "10-year maximum term stock option to purchase 20,264,042 shares of Tesla's common stock, divided equally among 12 separate tranches that are each equivalent to 1% of the issued and outstanding shares of Tesla's common stock," that would vest only if the company hit a combination of market-capitalization, revenue, and profitability milestones and Musk remained at the helm.

The first of those milestones would be a combination of Tesla reaching a market capitalization of $100 billion and either revenue of $20 billion or earnings of $1.5 billion (formally, adjusted earnings before interest, taxes, depreciation, and amortization, or EBITDA). According to the company's earnings report for the first quarter of 2019, it has hit those second two.

The next two operational milestones would be annualized revenue of $35 billion or earnings of $3 billion. Wednesday's second-quarter earnings report could shed light on how far Tesla has to go to hit those marks.

However, as the first market-capitalization goal is more than double Tesla's market capitalization as of Thursday, the company has not hit these goals, and so none of Musk's stock options under the compensation plan has vested.

The Times said in May that the compensation plan was intended to ensure Musk's long-term dedication to Tesla's growth and profitability, quoting the company's announcement that said it would "incentivize and motivate Mr. Musk to continue to not only lead Tesla over the long-term, but particularly in light of his other business interests, to devote his time and energy in doing so."

Several commentators at the time noted the unusual nature of the compensation package. Business Insider's Troy Wolverton reported that because Musk controlled a large amount of Tesla's stock, he already had strong incentives to boost the company's market cap.

Read more: 5 reasons Tesla is probably poised for a rebound

Tesla said in its 2019 proxy statement, filed with the SEC in 2018, that it compensated Musk with stock options worth an estimated $2,283,988,504 as part of the 2018 compensation plan. That value, on page 55 of the statement, was calculated in line with the SEC's accounting rules for equity-based compensation.

The reported $2.3 billion value of the stock options is from Tesla's estimates of what the options could be worth, based on how the company's stock price evolves. The proxy statement said that estimate did "not necessarily correspond to the actual value that may be recognized by the named executive officers, which depends, among other things, on the market value of our common stock."

Tesla said in the proxy statement that it was "required to report pursuant to applicable SEC rules any stock option grants to Mr. Musk at values determined as of their respective grant dates and which are driven by certain assumptions" laid out in Financial Accounting Standards Board guidelines.

That is, SEC rules require Tesla to report a measure of the market value of the unvested options from Musk's compensation plan, following standard accounting rules for CEO pay.

But the company said that under the terms of the compensation plan - and as pointed out above - none of those shares had vested, with the first tranche vesting only if Tesla first hits a market capitalization of $100 billion and one of the revenue and profitability goals is achieved.

The proxy letter includes, in addition to the unvested stock-option compensation, a $56,380 salary, following California's minimum-wage law. Tesla said that Musk had "not accepted his salary in the amounts of $56,380, $49,920 and $45,936 for 2018, 2017 and 2016, respectively." Musk has traditionally refused his annual paychecks from Tesla.

What gets reported can be different from what practically happens

In the proxy statement, Tesla pointed out the difference between the compensation level it reported and Musk's actual financial gain:

"As a result, there may be a significant disconnect between what is reported as compensation for Mr. Musk in a given year in such sections and the value actually realized as compensation in that year or over a period of time."

The company also reiterated the long-term, performance-based nature of Musk's compensation:

"Moreover, the vast majority of compensation in respect of past stock option grants to Mr. Musk, including the 2012 CEO Performance Award and the 2018 CEO Performance Award, were incentives for future performance and their value is realizable only if Tesla's stock price appreciates compared to the dates of the grants, and the Company achieves applicable vesting requirements."

To put that all together: Tesla reported to the SEC that it awarded stock options worth an estimated $2.3 billion to Musk in 2018 as part of the long-term compensation plan, but he cannot actually benefit from those options until the company hits at least one of its ambitious goals.

Courtney Yu, the director of research at Equilar, the executive-compensation and corporate-governance data firm that worked with The Times on its ranking of CEO pay, explained the situation in an email to Business Insider.

"While the SEC requires a certain calculation, such as using the grant-date fair value of unvested equity awards granted, this often doesn't reflect what the executive actually receives once stock awards are vested or options are exercised," Yu wrote.

Yu emphasized the contingent nature of the reported CEO pay.

"When it's all said and done, Elon Musk could realize all $2.3 billion of that option award, or he could realize nothing because the company doesn't meet performance goals," he said.

Yu also said a compensation measure including the grant-date value of unvested equity, as reported to the SEC, was still a useful metric for comparing CEO pay between companies "because it's a standardized calculation across the board."

Companies often publish other measures of CEO pay alongside the compensation reported according to SEC guidelines in order to give a fuller sense of what executives earn.

"However, it's also pretty common for companies to provide alternative calculations, such as the value of vested stock awards and exercised options, because they think this provides a better picture into what a CEO really makes," Yu wrote.

This divide is pretty common

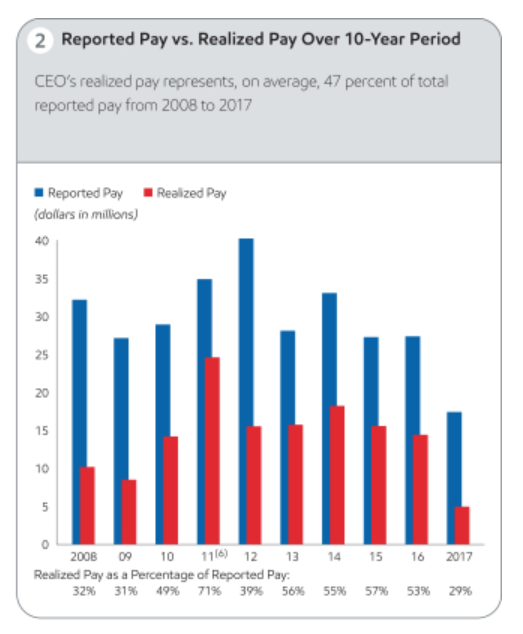

As an example of another company showing both reported compensation under SEC rules and the actual realized compensation for a CEO, Yu directed us to ExxonMobil's 2018 proxy statement, which included a chart showing that the realized value of executive compensation tended to be much lower than the reported compensation:

The chart illustrates how the reported compensation for ExxonMobil's CEOs over the past decade - roughly analogous to the $2.3 billion reported by Tesla - paints a very different picture from the realized pay that the oil company's CEOs actually received each year.

In 2017, CEO Darren Woods actually realized just 29% of his roughly $17 million in reported compensation. From 2008 to 2017, the average realized pay was just shy of half of the average reported pay.

Tesla's compensation plan for Musk remains different because of the high potential value for Musk and the extremely ambitious performance goals attached to that compensation. The basic split between what a company is required to report to the SEC and its CEO's actual increase in net worth is not uncommon among big corporations.

While the reported compensation is stunningly high, the nuances of how corporate CEOs are paid mean that Musk may end up gaining no real value in the form of actual new Tesla shares from those billions of dollars' worth of options.